Ok Zoomer

Breaking the internet and staying sane in lockdown

fHappy Sunday. Reporting live from Lockdown: California. The volume is turned down on most issues in tech not related to the current situation, and Zoom is arguably the most interesting company emerging from this saga.

The social animal

The past few months have been an incredible ride for Zoom. Since Wuhan, the stock has doubled despite market meltdown. In some tech-y circles, Zoom is approaching verb status. The company has pulled a reverse-Slack, jumping from Enterprise into consumer. A few of the use cases I’ve encountered in the past week

Zoom yoga classes - support the workers who are struggling to work from home

Zoom happy hour

Zoom card games

Zoom dates are apparently becoming a thing

and yes, we had our first Zoom porn attack

Zoom is seemingly dominating the entire world at once, both consumer and enterprise. Can this possibly continue?

Why is Zoom successful?

The bizarre component to this story is that Zoom broke all of the rules. Video conferencing is a large, obvious category. Cisco Webex was founded in 1995. Deep- pocketed should have solved this years ago. So why is Zoom winning?

Zoom “just works” in a way reminiscent of Apple. I have used several other video conferencing tools, none of which is terribly consistent.

Zoom makes it very easy to join someone’s meeting. They have removed the friction of signing up.

Zoom in-office technology is incredible. I can share my screen, and the software knows which room I am in. Feels magical.

Precedents

It is hard to find any sort of precedent for Zoom, not only because of the rarity of pandemics. Google, Facebook, and Apple dominate consumer markets but haven’t succeeded nearly as much in the enterprise. Amazon succeeds in both, but these are arguably two distinct companies not one offering. The only workable analogy is probably heyday Microsoft in the 1990s. This example highlights many of the risks for Zoom moving forward.

Zoom risks

As the use case for Zoom multiply, so will the competitive pressures. Video chat and communication are strategic and core not just to enterprise technology, but consumer tech as well.

Zoom is encroaching on: Apple, Facebook, Slack, Cisco, BlueJeans, Google, Houseparty and many more. That list is trillions of dollars of market cap, as well as many of the best engineers on the planet.

Zoom has a challenge making money from the consumer side. Their pricing model is geared to enterprise sales. Many of the consumer giants will not be charging anything.

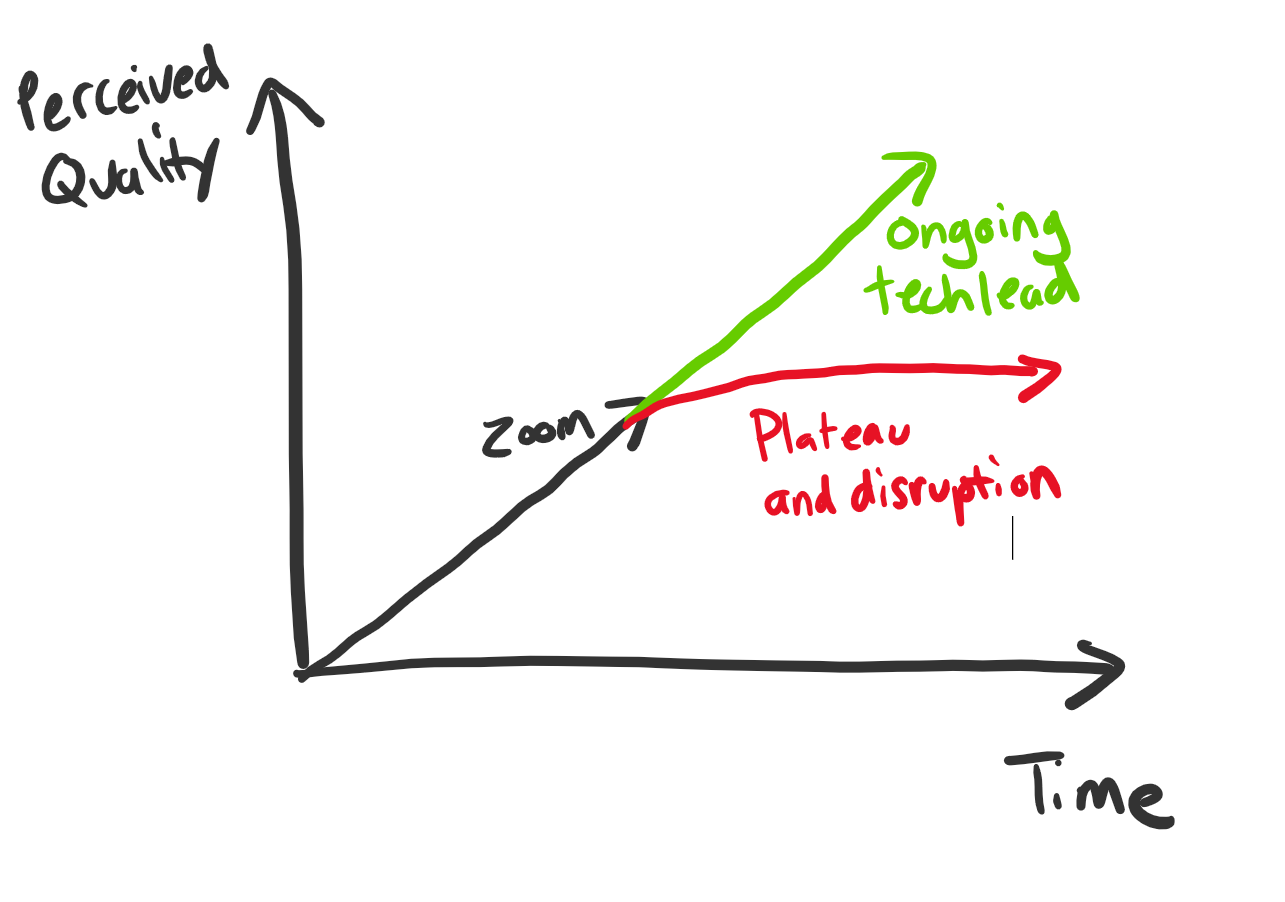

Zoom currently has a technological edge. Potentially the most important question for Zoom is which curve on the graph below applies moving forward. Will they be able to improve and maintain an edge in perceived quality? Or does video conferencing plateau, enabling others to catch up?

Said another way: what is the moat around Zoom’s business? Perhaps core technology for some unknown length of time. Zoom Rooms (their real world installation) applies only to enterprises. There is a social component to Zoom, but we don’t see the same type of network effect as past giants.

Paths forward

I will outline a few different paths forward for Zoom in descending order of probability.

The most obvious case is the most likely in my opinion. Zoom maintains laser-focus on the enterprise market. Corona gives a massive tailwind to video conferencing. Zoom is the main beneficiary of it in brand/name recognition and gains major momentum in their core business. Zoom is temporarily the default platform for all video use cases, and eventually standalone consumer applications poach much of the specialized consumer activity.

Zoom could achieve “verb” status like Google and Uber (and Xerox/Kleenex as nouns). Perhaps this crisis ingrains Zoom permanently in the collective zeitgeist. Zoom’s solution works well enough for most video conferencing use cases, with a handful of specialized applications like Telemedicine separating off. While I find this less likely than the above case, it wouldn’t require much additional effort. The main challenge for Zoom would be a pricing/packaging model for events/creators/small-groups that maintains the low-friction adoption while monetizing.

One thing missing from a Microsoft-esque dominance of video conferencing is some sort of platform or network effect. I consider it reckless for Zoom to license their video technology to enterprise players, but Zoom as consumer tech platform is one way to address the consumer market. Think of “powered by Intel” from the Wintel era. We are certainly going to see an explosion of video applications in the near future. Why should all of these applications reinvent the wheel? Zoom has solved this problem at scale. Powered by Zoom would position Zoom as the Amazon Web Services for video conferencing. Take a tax out of all consumer video communications across the internet. Unlikely, but at least worth a thought.

If we want to get really out there and futuristic, this lockdown might be the push that VR needs. Perhaps the video conferencing era is a temporary stepping stone to a sci-fi future. VR appears further away than this, but Oculus is gaining steam. Facebook wants to drive towards this future as soon as they can. This would obviously bode poorly for Zoom.

The upcoming action in video

Zoom is certainly exciting, but they are the tip of the iceberg of whats coming

Someone needs a camera that integrates with a TV to do high-quality video conferencing for Zoom. Laptops are only a portion of the future potential.

Telemedicine is being freed from regulatory shackles. Regulatory issues will likely force a specialized solution here.

Thousands of quarantined fitness instructors are taking to Zoom and social media to post workouts and lead classes. I will write more about home fitness soon, but Peloton is just the beginning here.

Students of all ages are being educated over Zoom. This might be the long-awaited catalyst for online education. Particularly in the face of a student loan crisis and Harvard laying off hourly workers despite a $40b endowment. I suspect we will find less of a educational difference and more cost savings than universities would like.

Dating apps have prioritized photos and text. One of the major dating apps will go video-first to differentiate in a crowded field.

Lastly, MeetUp and Eventbrite but for video events. It seems evident that one of these two would be able to quickly capitalize. There is a window of opportunity here as well to give it a shot.