Investigating the Coinbase P/E ratio

Investigating the Coinbase P/E ratio

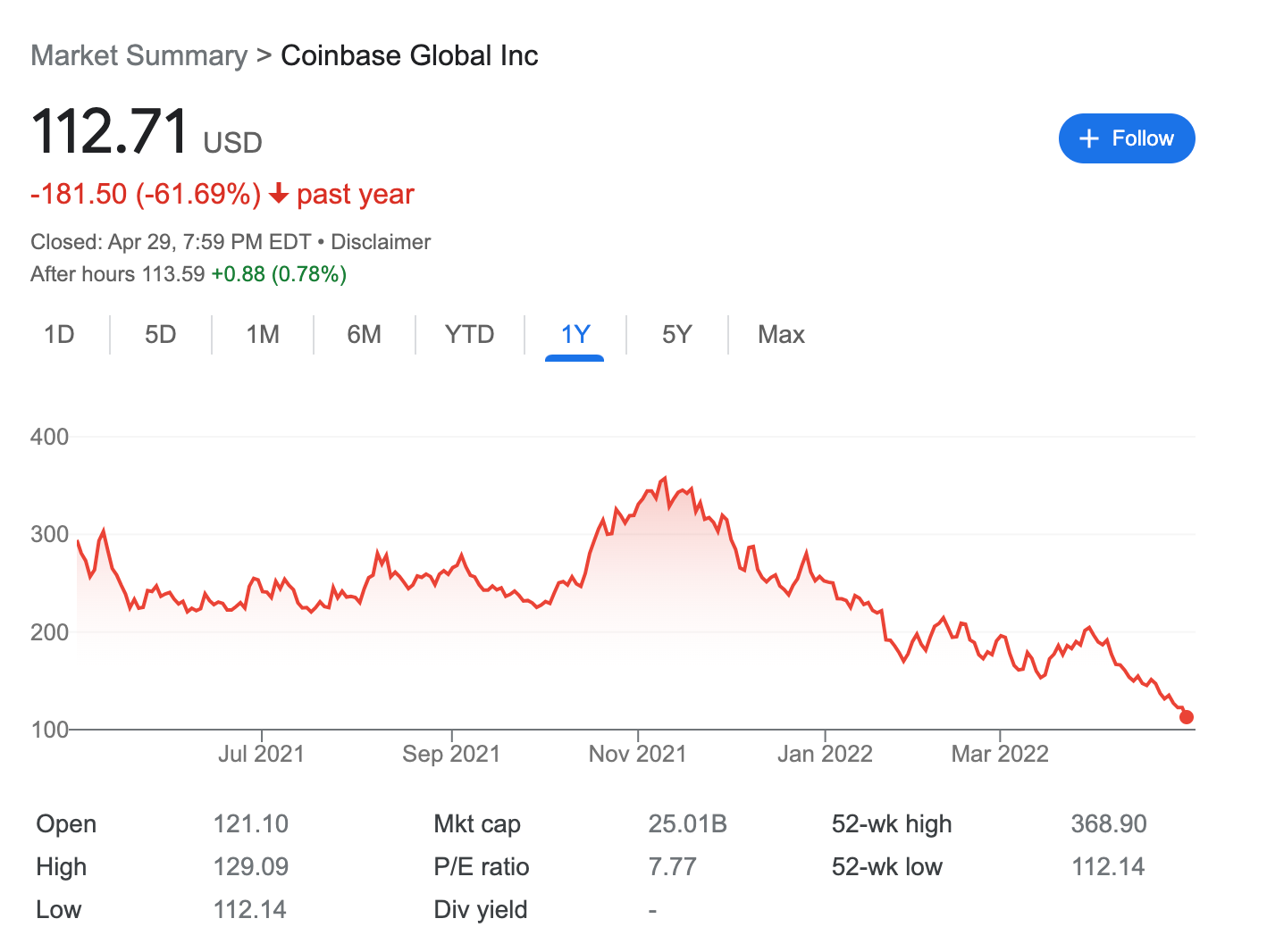

With the Nasdaq and startup valuations down so much, it is unsurprising to see the formerly red-hot Coinbase stock also down substantially from all-time highs. Coinbase stands out to me because unlike a Peloton or an Opendoor, the company is profitable and growing at a healthy clip. Q4 Revenue was reported at $2.5 billion, they generated nearly $850 million in net income, and both metrics were growing over 300% YoY. Yet Coinbase stock is down like a money-losing growth stock, and it trades for a significantly lower earnings multiple (7.8) than IBM (21) and Oracle (28).

Potential Culprits

The first issue for Coinbase is that competition continues to proliferate. While they can likely claim to be the premier US exchange, they are a distant has-been in trading volumes compared to Binance. Binance is a problematic entity, but other competition could be hitting Coinbase particularly hard with their best customers.

The lifeblood of a trading marketplace is the market makers and institutions. FTX is heavily courting this segment, as well as expanding into the US retail market.

Crypto die-hards are able to move their crypto off of Coinbase and trade on decentralized exchanges like UniSwap. Coinbase had a spat with the SEC over a lending product, which prevents them from touching much of the wild west of crypto. To access these services, one must leave the Coinbase mothership.

That leaves ‘retail’ - now feeling the pinch of higher gas prices, the end of stimulus checks, and paper losses on their $50k+ bitcoin purchases.

The second related issue is economics. Per CoinMarketCap, 6 different exchanges traded at least $100MM of bitcoin in the past 24 hours. I already mentioned that Binance's volume is nearly seven times that of Coinbase. Another issue here is that trading fees should begin to march towards ~zero with this much competition. After all, crypto tokens are fungible, uncensorable, and able to be sent across the internet instantly. Microeconomics eventually has to kick in.

There is an inherent contradiction in the current Coinbase business model. Cryptocurrencies are too volatile to be widely used in the economy. Stable cryptocurrencies would not be interesting for trading and speculating. Much like the maturation of Coinbase users allows them to trade on Uniswap, the maturation of Crypto is very bad for the current Coinbase business model yet the immaturity of crypto puts a ceiling on adoption.

Future Coinbase business models are not yet ready for prime time. The much-hyped NFT marketplace is off to a slow start. I don’t blame the Coinbase team here, NFT volume is trailing off quickly. I suspect inflated prices in the crypto AND stock markets created a wealth effect that justified buying ape jpegs. The jury is out on the long-run value of NFTs, but I suspect short-term pain looms. I wrote a while back about the larger vision of Coinbase and others to become banks. The SEC and other regulators seem significantly less friendly to that vision, meanwhile Goldman Sachs minted its first loan against bitcoin holdings.

So where should Coinbase focus? I would go after

Stablecoins (They are involved with USDC) - Stripe is showing the path forward here. This can solve real use cases.

Payments - They should partner with Square, Stripe and others to help drive mass adoption of stablecoin payments.

Focus on a few core cryptos and the crypto-bank vision. That likely means playing nice and making some sacrifices.

This is a much less exciting long-term business, but it seems far more stable. Coinbase is seemingly still in the best regards of the US regulators. Stablecoins will most certainly be reined in, benefitting the well-connected. Trading revenues just can’t be sustainable long-term. NFTs are a wild-card.

Brief Twitter comment

The discourse on Twitter about Twitter has been frustrating in the past week. The two sides are talking past each other. Is ‘free speech’ a perfectly neat definition? No. Does ‘free speech’ mean anything goes? No, the 1st amendment has a fair bit of case law about specific examples to the contrary. I think a more helpful framing is to break up the monolith of problematic speech into buckets. For example

Financial claims are regulated

Claims about the efficacy of medications are regulated

Incitement to violence is also regulated

Speech by an individual is very different than speech by a bot

Speech coordinated by a nation-state is a different bucket

A lot of problematic content can clearly still be covered even under a Musk-ian free speech regime. The clear sore spots will still be politics and culture war issues.